The luxury brand M&A index is released and see who is most promising to win China's LVMH

In 2017, the luxury goods industry continued to be favored by capital. In addition to the growth of large luxury goods groups through mergers and acquisitions, foreign capital in many countries and regions was also invested in this industry. In 2017, there were many high-quality brands and assets in the European and American markets. High-profile luxury brands were sold by capital for various reasons, attracting many competitions. With the continuous development of the Internet industry and the strong consumption power of millennials, high-quality luxury goods e-commerce has won the favor of capital. At the same time, Chinese capital has repeatedly participated in the bidding of international brands, and is gradually expanding the territory of the world luxury goods sector.

The global luxury goods industry mergers and acquisitions "fighting" transactions amounted to hundreds of billions of yuan

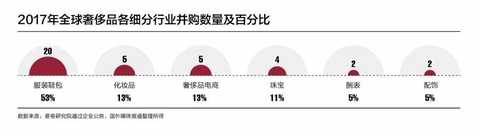

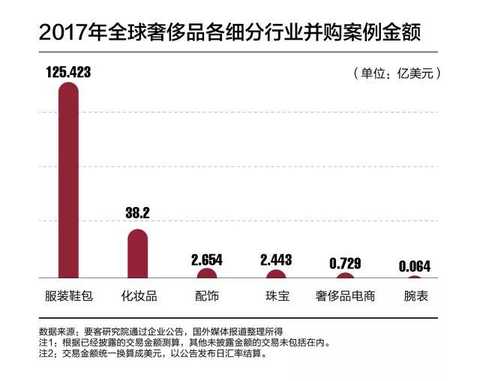

In 2017, there were 38 mergers and acquisitions in the luxury goods industry worldwide. The total transaction amount was approximately US$16.955 billion, including 21 for the apparel and footwear brand industry and 4 for the jewelry industry. For the two cases, the cosmetics industry acquired 5, the accessories category was 2, and the online e-commerce platform was 4. The largest single purchase was for LVMH to acquire the entire share capital of Christian Dior Couture, a high fashion business of the Christian Dior Group, for €6.5 billion. [The Visitors Research Institute is based on the transaction amount disclosed in 2017 and is uniformly measured in US dollars (based on the exchange rate of the announcement date). Other undisclosed transactions are not included. 】

Global luxury industry mergers and acquisitions characteristics

1. Five luxury goods groups, only LVMH Group is active

In the luxury goods sector in 2017, LVMH and its private equity fund L Catterton completed five acquisitions, including LVMH's 5% stake in Italian wool brand Loro Piana, acquisition of Australian swimwear brand Maaji, acquisition of Dior fashion department, acquisition of Korean glasses Part of the brand Gentle Monster, the acquisition of the Argentine underwear brand CaroCuore. Richemont Group completed the acquisition and acquired the Italian leather goods brand Serapian. Other luxury goods groups such as Kering Group, Hermes Group, and Swatch Group did not have any investment M&A events.

2. US light luxury group merger and acquisition integration is active

In 2017, the US Light Luxury Apparel Group was active in the luxury M&A industry. In May 2017, Coach Group announced the acquisition of US luxury luxury brand Kate Spade for US$2.4 billion, followed by US luxury luxury group Michael Kors for 896 million pounds (about 12 US$100 million acquired British luxury footwear brand Jimmy Choo. On the one hand, the downturn in the local retail market in North America has made the brand hope to increase the company's market value through mergers and acquisitions. On the other hand, the company hopes to attract new customers with a more diversified product portfolio.

3. Online e-commerce has become an investment hotspot

In 2017, many offline retailers chose to invest in online channels. In 2017, there were 4 cases of luxury e-commerce investment acquisitions. The famous French Galeries Lafayette department store announced in September that it acquired La Redoute, a French fashion and home e-commerce platform. Zheng Zhigang, the founder of K11 Art Mall and the founding father of Hong Kong New World Development Group, announced in December that he would invest in the US high-end fashion e-commerce Moda Operandi to further enhance its influence on digital lifestyle brands and platforms, with millennial consumers. Keep a consistent pace.

4. China's capital has exploded

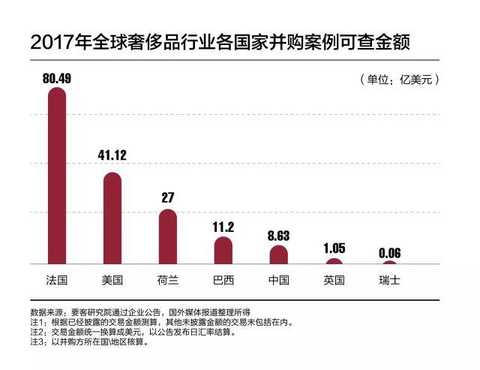

In 2017, China’s capital participated in a total of 12 mergers and acquisitions, including 9 cross-border acquisitions, totaling 863 million yuan, and more and more cross-industry acquisitions, among which foreign jewelry brands became hot spots for Chinese capital acquisition. The acquisition of Buccellati by Gangtai Group became the largest transaction amount in the 2017 China Capital Acquisition. In addition to the positive background of luxury goods consumption, Chinese companies are also seeking to change from the upstream to the downstream of the industrial chain. For example, Shandong Ruyi Group has successively acquired overseas fashion brands, allowing the local textile producers to complete the fashion brand operation group. The transformation, from fabric development and production to downstream high value-added links. This is also the embodiment of the “Made in China†to “Chinese Brand†upgrade process in a single enterprise.

Chinese capital becomes the global M&A protagonist of luxury brands

Shandong Ruyi is the best company to buy a brand in China.

In 2017, China Capital participated in a total of 12 investment and M&A cases in the luxury goods sector, with a transaction volume of approximately 6.3 billion yuan. Among them, there were 2 jewellery brand acquisitions, 5 clothing brand mergers and acquisitions, 1 crystal jewelry brand acquisition, 3 luxury brand Chinese agent acquisitions, and 1 overseas luxury electricity supplier investment. The largest single purchase was the acquisition of 85% of Buccellati by Gangtai Group, which reached 195.5 million euros.

In recent years, China's capital luxury goods industry mergers and acquisitions have been driven by three aspects, including the basic national policy of the Chinese government to encourage Chinese enterprises to “go globalâ€; the internal driving of consumption upgrading drives the demand for industrial upgrading; enterprises hope to expand the market value.

For a long time, domestic fashion enterprises have started from the mass consumer market. The products have formed a low-end impression in the hearts of Chinese consumers. It is difficult to build high-end brands with their own strength. Therefore, under the encouragement of the basic national policy of “going outâ€, domestic consumption is utilized. The trend of upgrading meets the market demand and becomes an effective way to upgrade the industry. Through the acquisition of luxury brands, these companies can not only make profits through the brand itself, but also gain the design and research and development capabilities of the world's leading luxury goods companies; cover the distribution network of the country where the target country is located, and gain direct access to the local market; gain international first-class luxury The company's management model, quality standards, store maintenance, logistics system and advertising communication experience; gained a talent team and staff training system. At the same time, these “going out†Chinese companies such as Shandong Ruyi, Qipirang and Tongling Jewelry are almost all domestic listed companies, and overseas mergers and acquisitions are also very beneficial to their market value management.

Chinese capital luxury brand M&A characteristics

1. The acquisition of the underlying brand is becoming more and more famous.

In the luxury brands acquired by China Capital in 2017, there were luxury brands such as Karl Lagerfeld and Yageshidan. The international popularity of the purchased brands has improved compared with the previous two years.

2. The acquisition of the brand is concentrated in Europe

Chinese capital favors European brands. In 2017, luxury brands of Chinese capital mergers and acquisitions came from Europe, among which Italian and French brands were most favored by Chinese capital. Under the influence of the European debt crisis, many luxury brands, especially those with relatively weak economic foundations, have selling intentions, which is an unprecedented opportunity for Chinese companies.

3. Jewelry brands are concerned by Chinese capital

The jewellery brand became the core project of China's capital overseas luxury brand mergers and acquisitions in 2017. The mergers and acquisitions involved include the acquisition of 81% of Joaillerie Leyse Freres SA by Tongling Jewelry and the acquisition of 85% of the Italian jewellery brand Buccellati by Gangtai Group. In China, consumer jewellery consumption is in the midst of changing the way from buying materials to buying brands and buying designs. China's domestic jewellery brands are aging and iteratively slow to meet the rising market demand. China's high-end jewellery market is gradually becoming more and more popular. Occupied by Cartier, Tiffany and other big names, Chinese companies hope to complete the market after the transformation and upgrading of jewelry consumption through acquisition. Another reason is that high-end jewellery brands have a perfect brand matrix in Lifeng and LVMH Groups, brands are too dense, and the positioning between brands is difficult to open the difference. The target consumer groups have high overlap, and internal competition is inevitable. Many family-owned jewellery brands are more willing to look at emerging capital markets like China.

Chinese corporate luxury brand M&A index:

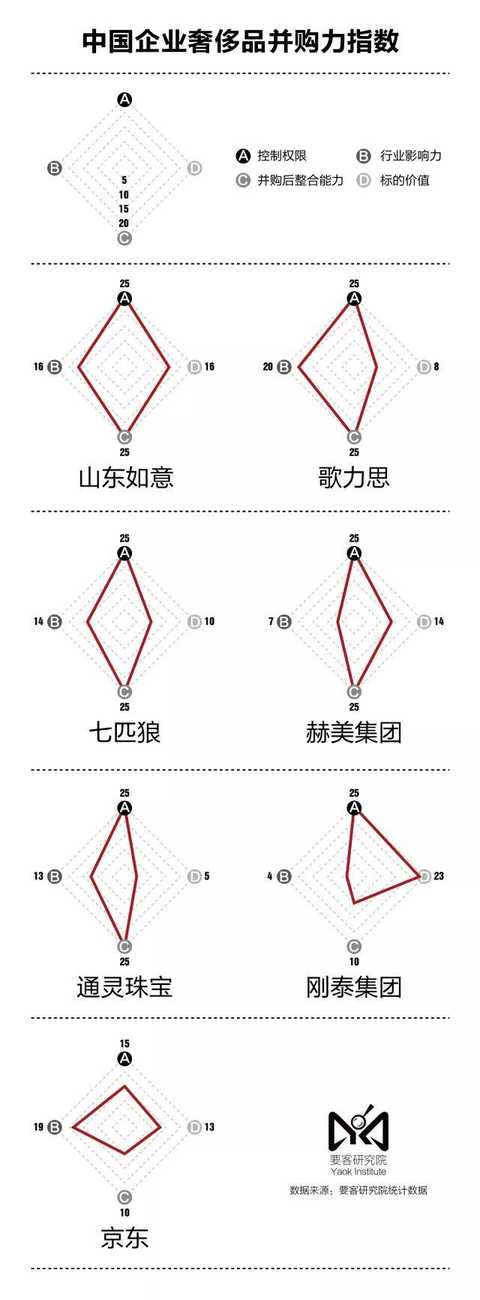

Shandong Ruyi bought the most, just bought the most expensive

In order to better analyze the case of Chinese companies' luxury mergers and acquisitions, the Guest Research Institute released the Chinese company's luxury goods M&A index. The Chinese company's luxury goods M&A index is an indicator reflecting the performance of Chinese companies in the M&A market. It is judged in terms of the subject control authority, the target value, the post-merger integration capability, and the M&A industry influence. Merger and acquisition authority refers to the proportion of the equity of the M&A enterprise in the target enterprise. The target value includes the target purchase price, the target market position and the target pre-acquisition operating status. The post-merger integration capability is measured by whether cross-domain acquisitions, whether to promote upstream and downstream integration of buyers, and whether there is a professional team operation after the merger. The influence of the M&A industry is measured by the exposure of the acquisition industry and the change in share price caused by mergers and acquisitions. Among them, Hongyi Capital, Yan Capital and Fosun International did not appear on the list due to lack of key data.

Editor in charge: Xu Yuehua

Polyester Mesh Series,Polyester Mesh,Polyester Spiral Dryer Mesh,Polyester Spiral Dryer Fabric

Dongguan Yexing Paper Felt&Wire Co.,LTD , https://www.yexingfelt.com